- HX Daily

- Posts

- HX Weekly: May 11 - May 15, 2026

HX Weekly: May 11 - May 15, 2026

The Next Huge Momentum Trade Is Here

Hello reader, welcome to the latest issue of HX Weekly!

Our goal with HX Weekly is to highlight both timely and timeless research. Most often this involves sharing a new note along with one we have written in the past. (In addition to our biography piece...)

Today, we are going to share two pieces that recently ran in our free newsletter Truth and Trends with Paradigm Press Group.

Both involve the emergence of a strong momentum trend in the current market environment particularly focused around semiconductor stocks. We think this trend creates a lot of opportunity but even more risk.

The first piece is one we ran last week and the second pieces is one our colleague Nick Riso shared earlier this week.

Enjoy.

Thoughts on the Market

The MU-mentum Trap: When Good Trades Go Bad

There's a moment in every momentum cycle when a stock stops trading like a business and starts trading like a movement.

Right now, we’re entering that phase in DRAM and memory-chip stocks.

Momentum across the group has been building rapidly.

And stocks tied to memory demand like Micron are moving with the kind of aggressive price action that often appears late in a momentum cycle.

This is the point of the cycle when things get really exciting — but it’s also when things get incredibly dangerous.

Momentum investing and the rapid thematic rotations that come with it are still deeply misunderstood by most investors.

Most people think it simply means buying stocks that are going up. But that's only part of the story.

Real momentum investing is about psychology and narratives.

It’s also about institutional money piling into a theme so aggressively that the trade itself becomes more important than the underlying fundamentals.

And once that happens, the cycle can accelerate very quickly.

A stock moves higher, headlines follow, and more investors notice…

Then analysts raise price targets, financial television starts covering the theme every day, and social media amplifies the move.

Retail investors rush in, afraid of missing the next big thing. Before long, the entire sector is moving together regardless of quality.

At that point, the market often stops asking whether a company is good and starts asking whether it's part of the hot trade.

That distinction matters far more than most investors realize.

Because in the early stages of a momentum cycle, stocks usually rise for legitimate reasons. The company executes well. Earnings improve. Demand strengthens.

The underlying story makes sense. But eventually, something changes.

The stock transforms from a good story into a good trade. Once that happens, price action itself becomes the catalyst.

Most Investors Don’t Get the Momentum Game

One of the biggest misconceptions about momentum investing is the idea that you need to catch the trade at the very beginning to make money.

You don’t.

In fact, many momentum trades generate their biggest gains in the middle innings after the trend is already clearly established.

If you think about it like a baseball game, it’s perfectly fine to miss the first few innings and still enjoy the game. The real problem is figuring out when the game is about to end.

That’s where investors get into trouble.

Because momentum trades tend to end the same way they begin: suddenly.

The same psychology that pushes stocks vertically higher can reverse just as quickly once institutional money starts rotating into a new theme.

And when that rotation begins, investors who entered late often find themselves holding stocks that fall much faster than they rose.

That’s especially true when speculative names become attached to the trade.

We saw this exact dynamic play out over the last year in nuclear and power stocks.

When the AI Trade Took Over Everything

One of my favorite stocks during that period was Talen Energy. In fact, I still love this stock.

I originally called the trade early (back in March of 2025) because I believed the business itself was compelling.

Power demand was increasing, AI infrastructure was growing rapidly, and electricity was becoming one of the most important bottlenecks across the technology sector.

The thesis made sense.

Initially, Talen traded like a quality business with improving fundamentals. But as the AI infrastructure boom accelerated, something else happened.

The market stopped viewing these companies individually and started lumping them together under one massive momentum umbrella: anything related to AI power demand.

Suddenly, it didn’t matter whether a company had strong operations, real cash flow, or proven execution.

If it had exposure to nuclear, power generation, uranium, or electricity demand, investors piled in aggressively.

The entire sector went vertical.

High-quality businesses rallied. Speculative businesses rallied. Pre-revenue companies rallied.

Anything tied to nuclear energy suddenly became “must own.”

That included names like Oklo, which fundamentally were nowhere near the quality level of a company like Talen.

But during peak momentum cycles, quality temporarily ceases to matter. The theme becomes the trade. And for a while, that trade can feel unstoppable.

The Problem With Momentum

The problem, of course, is that momentum works both ways. As the old expression goes, "live by the sword, die by the sword."

Eventually, the AI trade became overheated.

Valuations are stretched too far. RSI levels across the sector reach extreme levels. Every conversation on Wall Street revolves around the same themes.

That’s usually when institutional money quietly begins rotating elsewhere.

And once that rotation started, the downturn across nuclear and power stocks was fast and brutal.

The same momentum that pushed these names sharply higher suddenly accelerated them lower. Investors who chased the trade late found themselves trapped almost immediately.

Now, here’s the important distinction.

I never lost conviction in Talen because I wasn’t owning it strictly as a momentum trade.

I believed in the underlying business and the long-term demand story.

And I understood that temporary market rotations don’t change the quality of a strong company.

So, while Talen entered a healthy consolidation period, I was comfortable holding through the volatility.

Today, the stock is finally emerging from its consolidation phase and regaining strength.

But many investors holding lower-quality speculative names never recovered.

They didn’t understand the difference between a good business and a good trade. And when the game ended and the theme broke, their portfolios broke with it.

That brings me to why I’m writing this today.

The Next Huge Momentum Trade Is Here

I believe we are seeing the exact same setup developing right now in DRAM and memory chip stocks.

Companies like Micron Technology are absolutely legitimate businesses with real long-term tailwinds.

AI infrastructure demand is real. High-bandwidth memory demand is real. Data center growth is real. This is not a fake story.

But what started as a strong standalone investment thesis is now evolving into a broader momentum trade.

And once that happens, sectors stop moving based purely on fundamentals. They start moving in response to crowd behavior.

You can already see the signs emerging throughout the group.

RSI levels have become elevated.

Retail participation has exploded.

Stocks tied to memory, DRAM, and AI infrastructure are all starting to move together in an increasingly aggressive fashion.

That doesn't mean these companies are bad businesses, far from it. But even great companies can become dangerously overheated stocks in the short term.

And that’s the part many investors fail to appreciate.

A stock can still be an excellent long-term investment while also being vulnerable to a sharp momentum-driven pullback.

What to Do About It

To be clear, I'm not telling you to panic-sell your Micron shares tomorrow morning. And I’m certainly not saying the long-term AI infrastructure story is over.

But if you’ve built substantial profits during this latest momentum run, it may be time to start trimming positions and protecting gains.

Because what goes up eventually cools off. Always.

Sometimes that cooling-off period is mild. Sometimes it's violent. But no momentum trade keeps rising forever.

And if you’re only now feeling the urge to jump into the DRAM ETF and memory stocks because the sector suddenly feels unstoppable, there’s a decent chance you’re entering the game in the later innings.

That’s exactly how FOMO works. It convinces investors that missing the trade is riskier than entering late.

In reality, entering late is often the biggest risk of all.

The smarter move is usually patience.

Wait for the excitement to cool down. Wait for the consolidation phase. Let the weak hands get shaken out.

Then come back and focus on the highest-quality survivors once the momentum resets itself.

Because the goal isn’t simply to catch the hottest trade.

It's to survive long enough to catch the next one, too.

You can check out the original post here: https://www.truthandtrends.com/posts/the-mu-mentum-trap-when-good-trades-go-bad

The Tell-Tape Heart

By Nick Riso

There’s a version of events in which Micron's stock price over the last three weeks reflects something real.

Analysts have been upgrading their targets. There's institutional conviction in the AI memory cycle. And the market is efficiently pricing a company whose chips sit at the center of the most consequential infrastructure buildout in a generation.

Everyone keeps saying that semiconductors are the oil of the 21st century, and Micron makes the refineries.

Last Friday, the stock was up 15% on the day, capping its best week in two decades. Currently, it's trading near all-time highs above $800.

MarketWatch noted that it was now worth more than JPMorgan, and CNBC called the rally parabolic.

The brokerage notes were falling over each other.

That version is clean and legible… and almost certainly wrong.

The actual mechanism driving Micron's price is sitting in the options tape. It has everything to do with arithmetic — and almost nothing to do with conviction.

Let’s Look Under the Hood

When you buy a call option on a stock, someone has to sell it to you.

That someone is almost always a market maker, a dealer whose entire business model depends on staying directionally neutral — on never actually caring whether the stock goes up or down.

To stay neutral after selling you a call, the dealer has to buy the underlying stock. Not because they want to, of course. But because their risk model requires it.

The amount they buy is determined by the option's delta, a measure of how much the option's value moves relative to the stock.

A call with a delta of 0.30 means the dealer buys 30 shares for every 100-share contract. As the stock rises and the call moves closer to being in the money, the delta increases and the dealer buys more shares.

As the stock rises further, they buy more still. They’re doing math, not making bets.

This is the mechanism. And it’s why the options market matters in Micron's case specifically.

When you have hundreds of thousands of people buying calls on the same stock in the same week, the dealers who sold those calls are collectively purchasing enormous quantities of the underlying shares.

It’s as simple as this…

The stock goes up. The calls get more valuable. More people buy calls. The dealers buy more stock. The stock goes up again. The people who bought calls last Monday feel vindicated and buy more this Monday. Around and around and around we go.

What makes this unstable is what happens when it stops.

The calls expire Friday afternoon. The dealers who were long Micron stock to hedge those calls no longer need to be, so they unwind.

If the crowd comes back Monday and reloads — and for 15 straight sessions they have — the hedge book rebuilds and the stock finds its footing.

But if they come back smaller, or if something spooks them, or if the expiration Friday is large enough that the unwind overwhelms the new buying, the stock loses the only thing that was actually holding it up.

There is no fundamental buyer waiting underneath. There is just the absence of a mechanical one.

Into the Numbers

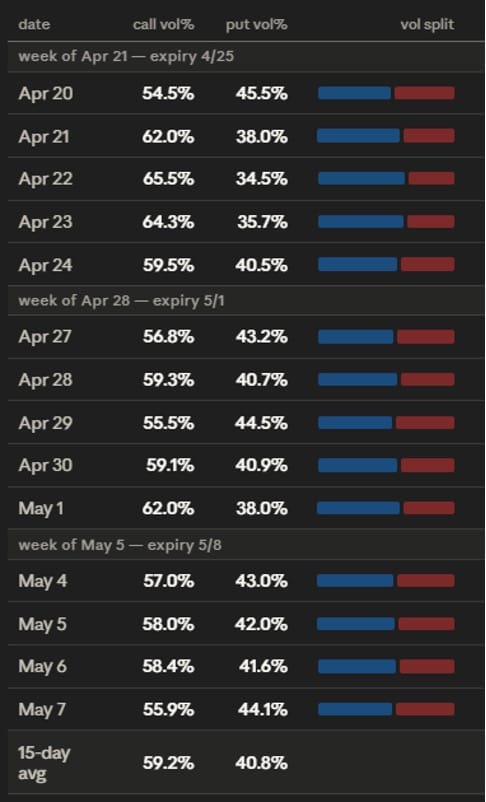

For 15 consecutive trading sessions (April 20–May 8), roughly half of all options volume on Micron expired that same Friday.

The number was 48% on April 20, a Monday. It was 51.9% on April 22, a Wednesday. On May 7, a Thursday, one day before expiration, it reached 57.3% — the highest reading in the entire dataset.

The crowd was accelerating exposure into expiration.

On May 8, 1.6 million contracts changed hands, the largest single session in the period. And 848,000 of them (53.1%) expired that afternoon.

Over the course of my analysis, this three-week period, the number never dropped below 47%.

Calls dominated volume every single day, averaging 59.2% of all contracts traded. Some days the skew was more dramatic — 65.5% on April 22, 62% on both April 21 and May 1.

There was not a single session in which puts led volume. To look at the tape, Micron was the most straightforwardly bullish major semiconductor in the market.

Everyone was buying upside. But there’s a wrinkle in this story.

We have to understand first and foremost that volume is what people do today.

Open interest is what they're still holding when the market closes. And open interest told a completely different story.

Puts outnumbered calls in open interest every single day.

The put-to-call ratio in open interest started the period at 1.109 on April 20 and ended it at 1.193 on May 7, grinding higher session by session without a single reversal.

On the days when call volume was most lopsided — when the tape looked most bullish — the put book underneath kept getting heavier. Every Friday, the weekly calls burned off. And every Monday, the puts were still there.

Not once did the two stories converge.

What this means is that two completely different groups of people have been participating in Micron's options market simultaneously. And they have been making opposite bets.

Two Camps

The first group is loud. You know who I mean…

They buy calls that expire Friday, generate the volume that moves across the tape, and create the dealer hedging flows that push the stock higher. Their wins are fast and visible. Their losses are total and weekly, and they come back anyway.

The second group is quiet. They don't show up in the volume numbers — they show up in the open interest, accumulated position by position over weeks, and they are overwhelmingly on the other side.

The question worth asking is which group has been paying more attention to the actual structure of what's happening.

Implied volatility (the market's expectation of future price movement baked into options prices) has been rising for three weeks alongside the stock.

This is the kind of thing that gets dismissed as a technical footnote but is actually one of the more reliable warning signs available.

When a bull market is healthy, volatility compresses as prices rise.

The move confirms the thesis. Uncertainty resolves and options get cheaper.

In Micron's market, the opposite has happened.

Volume-weighted average IV was 79.8% on April 20. By May 7, it was 100.5%, and it had been above 100% for multiple sessions. The market was pricing in bigger and bigger potential moves even as the crowd bought calls expecting the stock to grind higher in an orderly way.

These two things cannot both be right at the same time.

More telling than the level is the shape.

On April 20, near-term implied volatility (on contracts expiring within two weeks) was 79.6%. Far-term IV was 79.9%. The curve was flat, which is normal. By May 7, near-term IV was 105.4% and far-term IV was 84.4%.

The curve had inverted.

The market was pricing in more uncertainty for the next two weeks than for the next six months. This is a condition that resolves, and it resolves through price.

Then there is what happened on May 8, expiration Friday, the biggest session in the dataset.

The largest block trades that day were not calls.

They were puts — deep out-of-the-money puts, struck at $405, bought on the ask at implied volatilities between 164% and 171%. The largest single print was 8,442 contracts. Then 6,000 more at the same strike… Then 4,000 more.

Over 18,000 contracts in a cluster, all pointing the same direction, all paying extraordinary premiums for the right to profit from a move that would require Micron to fall sharply from where it was trading.

The delta on these contracts was essentially zero, and they weren’t hedges. A hedge is sized efficiently against a known risk. These were a bet, placed by someone who looked at the most bullish-looking tape in the semiconductor space and decided the risk worth paying for was catastrophic downside.

The last piece is the one that is hardest to dismiss.

Far-dated options — contracts expiring more than two weeks out, insulated from the weekly gamma noise, priced by people making longer-horizon decisions — averaged $1,732 per contract on April 20.

By May 7, the average had reached $8,848. A 5.1x increase in 15 trading days.

Far-dated options don't get that expensive because of retail momentum. They get that expensive because someone with a longer time horizon is making a considered decision to pay significantly more for exposure that won't resolve this Friday or next.

The near-term crowd got louder while the long-term crowd got more expensive.

They are not describing the same market.

Gamma squeezes are not unusual. Stocks get caught in them, run hard, and eventually the structure exhausts itself.

What is unusual about Micron is the duration, the consistency, and the scale of the divergence between what the volume says and what the open interest says — between what the crowd is doing and what the patient money underneath has been building for three weeks.

Micron is silver in 2025 leading up to the late January reckoning. Where precisely it is, we don’t exactly know. What we do know is that this doesn’t end well.

The crowd has been right about the direction. The question is whether they understand what has been generating it and what happens when it stops.

The calls expire on Friday. They always do.

The puts are still there on Monday morning. They always are.

At some point, those two facts are going to matter at the same time.

You can check out the original post here: https://www.truthandtrends.com/posts/the-tell-tape-heart

With momentum building in the stock market and the talk of a true "bubble" becoming more real, we thought we would share the thoughts of one of the greatest "bubble" investors of all-time - George Soros.

Enjoy and have a great weekend!

Market Wizard’s Wisdom

The Macro Master: Intellectual Insight of George Soros

A couple years ago, I had the opportunity to take my first real trip in many years.

Over my lifetime, I have visited fifty-three countries. I'm not sure my goal is to visit all of them before I die, but I certainly want to visit a lot of them.

For most of the last thirty years, I have been able to hit a new one or a few new ones every year. In the previous six years, though, I have not visited ANY new ones. Between work, COVID, and life – my travel has been curtailed.

After successfully launching HX Research earlier this year, I decided to visit Eastern Europe.

The first place I visited—and the one I was most excited to see—was Budapest, Hungary. I honestly know little about the place but have always been very intrigued by it.

As we walked around this ancient city, I thought about one of its natives, George Soros, who became one of the greatest investors of all time.

Most of you are familiar with Soros. His story is an incredible one.

He was born in Budapest in 1930 to a non-religious Jewish family. They stayed in the country and survived the horrific events of the Nazi occupation and the holocaust. There were over 550,000 Hungarian Jews who did not survive.

He left in 1947 and eventually attended the London School of Economics. After working at several merchant banks after graduation, he founded his first hedge fund—Double Eagle—in 1969. In 1970, he used it to start Soros Fund Management and changed the name of the fund to Quantum Fund.

Over the next four decades, Soros built one of the most legendary track records in investment history.

He has generated some controversy in recent years with his strong political advocacy.

While this has led to some detractors, no one can doubt his ability to use powerful intellect to master the global markets.

Soros is one of the investors who has most influenced my own strategies, but he is also one of the most difficult to understand.

Soros is not known for simple quotes. Here are a few of our favorites, along with our thoughts…

“It's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.”

Soros is known for his complex thoughts, but this is a simple and powerful trading insight.

We discuss this often when discussing our strategies. Everyone would prefer an approach that wins most of the time. Our TRADING strategies make money in over 70% of all our positions.

To make BIG money, though, you should aim for big returns. You also should manage your losses. This combination is how you compound wealth over time.

This is what we do in our INVESTING strategies. However, we will point out that most of our stocks make money there, too!

"Markets are constantly in a state of uncertainty and flux, and money is made by discounting the obvious and betting on the unexpected."

It isn't always what happens that is most important; rather, it is what happens relative to what investors THINK will happen.

Once an investor understands this concept, they are in a much better position to make money and manage risk.

The concept of expectations driving the market is an important jump to make to be successful.

“My peculiarity is that I don't have a particular style of investing or, more exactly, I try to change my style to fit the conditions.”

This is one of our favorites.

My partner Whitney Tilson once asked me what strategy we use in our investing and trading. I think he was expecting an answer like "value" or "growth.”

My answer was that I was a “make money” investor.

The environment changes, and your strategies need to adapt to be successful.

"The fact that a thesis is flawed does not mean that we should not invest in it as long as other people believe in it and there is a large group of people left to be convinced." The point was made by John Maynard Keynes when he compared the stock market to a beauty contest where the winner is not the most beautiful contestant but the one whom the greatest number of people consider beautiful. I have something significant to add: it pays to look for the flaws; if we find them, we are ahead of the game because we can limit our losses when the market also discovers what we already know. It is when we are unaware of what could go wrong that we have to worry.”

This is a more typical Soros quote. It also raises one of the most powerful concepts in investing: Soros's theory of "reflexivity.”

This is the idea that investor perceptions of the future can influence the outcome.

This insight can occur at key market points and with particular stocks. IF you can identify these points, you can make an absolute fortune!

We hope that you’ve enjoyed this week’s issue of HX Weekly…

What did you think of today's HX Weekly?Your feedback helps us create the best newsletter possible. |

Do you have any thoughts, questions, or feedback? Tell us more in the comment section or at [email protected].

Reply